Make reported data accessible

Data accessibility means making your sustainability data easy to see and easy to use.

You should plan to make your sustainability disclosures available to not only the regulatory bodies but also to other entities that may be interested in comparing your results with other results.

It is important to use a common standard when planning how to report your sustainability data. If companies do not use the same data structures when preparing their reports, it is difficult to analyse and compare the data.

XBRL standard and data accessibility

The XBRL standard enables companies to use a predefined list of codified terms to report their information. Thanks to that, it is possible to compare the data between companies and analyse the results.

When companies prepare their sustainability report in the XBRL standard, for each disclosure, they prepare two layers of information. The first layer is text, which presents the information, and the second layer is codified terms, which give specific details about the information.

To make the data reported in the XBRL standard available, companies only need to make sure to use the codified terms provided to them by standard setters and regulators. The first layer, text, can be custom and specific for the company.

Example

Three companies report their Green House Gas Emissions, Energy Consumed, and Total Energy Cost.

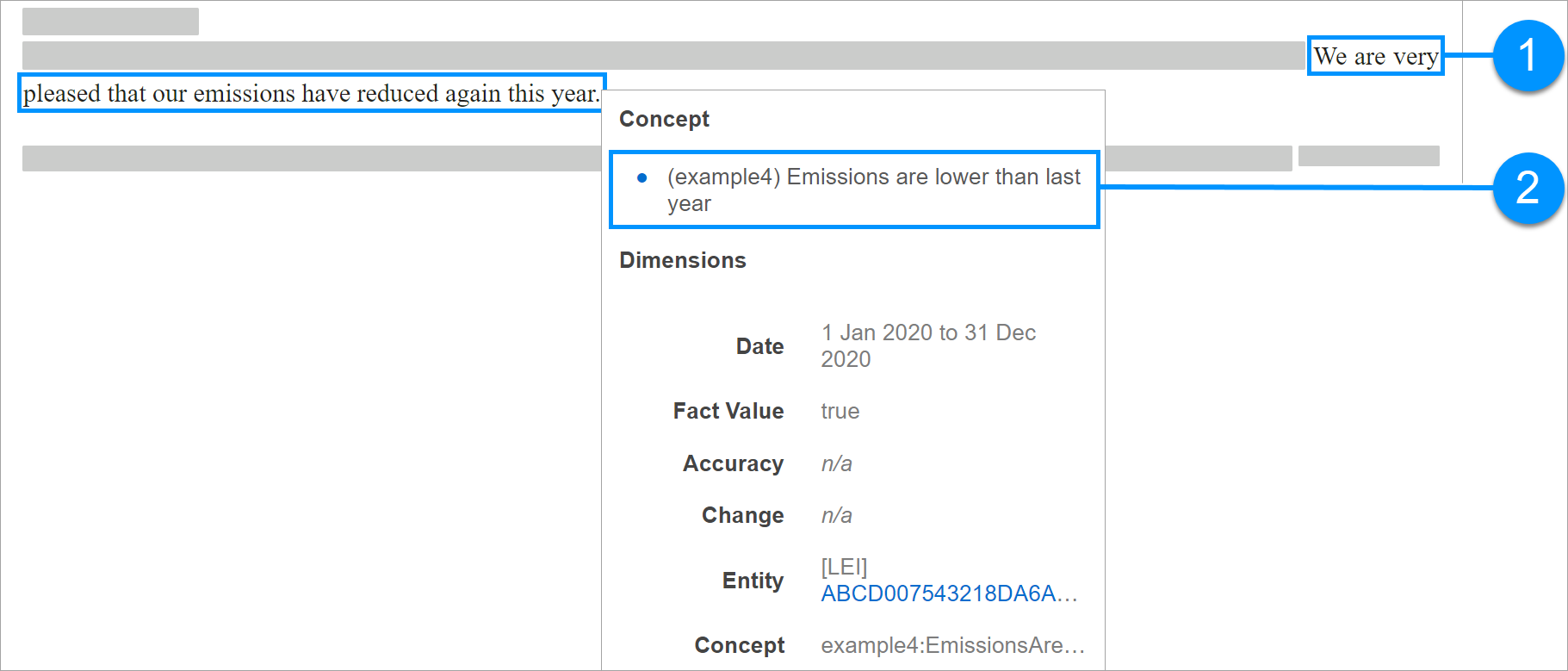

Here are the individual digital reports for each company, presented in the iXBRL format. If you click one of the facts in the report, you can see the XBRL taxonomy concept associated with that report fact.

CarMaker report (iXBRL format)

Cloud-ify report (iXBRL format)

OutSourcery report (iXBRL format)

Because all three companies used the taxonomy concepts provided to them by standard setters and regulators, the reports can be compared and analysed.

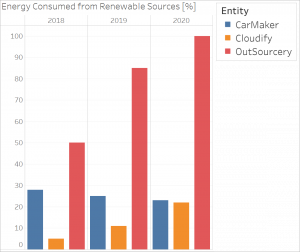

Here, you can see a chart with all three companies. We compared the values reported by each of the three companies against the (e1) Energy Consumed from Renewable Sources [%] taxonomy concept. As each company reported against that taxonomy concept for 2018, 2019 and 2020, we compared their values for each of those years.

Chart comparing the three companies (Tableau report)

More detail

XBRL taxonomies

The XBRL standard enables companies to use taxonomy to report their information. The iXBRL (Inline eXtensible Business Reporting Language) enables adding machine-readable taxonomy concepts to human-readable report facts.

| Item | Description |

|---|---|

|

Report fact |

|

Taxonomy concept |

The taxonomy is provided to companies by standard setters and regulators. The taxonomy should contain all the taxonomy concepts that data preparers need to prepare their report. If the taxonomy does not contain all the required concepts, the data preparer may use invalid concepts to report their data or add custom taxonomy concepts. Both actions have a negative impact on the data accessibility.

If companies prepare their reports using the taxonomy concepts provided, the XBRL standard enables the comparison of the same disclosures between different reports. It is possible, for example, to use BI software to analyse the data and have a broader view of a particular data sector.

Taxonomy extensions

Standard setters and regulators are responsible for providing taxonomies to companies that report their sustainability data. The provided taxonomy should be complete and predict the company’s needs.

XBRL helps companies to create their own concepts and include them in their reports. However, these company-specific concepts limit the reports’ comparability as they are unique to that one company.

Extensions are useful when a data preparer must provide and tag more specific information than currently captured by the standard setter taxonomy. However, data collection regimes that avoid extension are lower cost for data preparers.

We encourage standards setters to develop collaboration and governance processes to ensure their taxonomies continue to meet market requirements.

Creation and use of XBRL taxonomies is best done in conjunction with certified XBRL software, in particular with a validating processor.

Learn more about available certified software

Data validation

XBRL helps technical implementers by making it easy to validate their sustainability reports. XBRL enables verifying if the reports use the correct syntax and if both report facts and taxonomy concepts use the correct data format. Thanks to that, companies can ensure that the reported data is valid, which means it can be compared and analysed.

The core XBRL specifications define validation constraints which XBRL processors must impose on all XBRL reports. These enforce not only basic syntactical checks but also ensure that the reports comply with the definitions in the taxonomy. The validation checks include:

-

Data types

All definitions of taxonomy concepts are associated with a data type that enforces basic validation of the format of reported values. For example, ensuring that strings are not reported against concepts which should take numeric values. At a technical level, XBRL reuses the XML Schema data type system. The standard defines a wide range of base data types, but the Data Type Registry 1.x allows for the collaborative development, rapid review, publication and on-going use of additional specialised data constraints. -

Dimensions

Taxonomies can associate dimensions with concept definitions, which means it is possible to control which dimensions may be used with particular concepts. -

Calculations

Taxonomies can capture basic summation relationships between taxonomy concepts which is checked during the validation process. As the scope of calculations that can be defined in this way is limited, many implementations choose to use Formula for all calculation constraints. -

Units

The XBRL 2.1 specification requires that report facts for taxonomy concepts with a monetary data type use particular units based on the ISO 4217 currency code standard. More general constraints between data types and units can be defined in the Units Registry 1.0.

Many reporting domains impose more complex constraints on reported data. For example, the value of one reported fact may control whether another fact is required, or there may be more calculation constraints between facts.

The Formula specification makes it possible to capture such constraints in an XBRL taxonomy in a standardised format. This makes XBRL taxonomies immensely powerful, as a regulator can publish a single artefact that completely defines the reporting requirements for a particular domain including validation rules that can be executed by any compatible software.