Use concepts from external taxonomies

The XBRL standard allows data preparers to use a concept from another taxonomy in their reports.

Sustainability reports can include data that is not sustainability data. For example, the sustainability standard may require financial data to be included in a financial report. This data can be copied from the financial report into the sustainability report, but it will not contain the data attributes, like units, dates, or currency. These attributes are defined in the facts reported against taxonomy concepts used to create the financial report. Referencing the taxonomy used for the financial report in your report is a shortcut that saves you time.

Advantages of referencing other taxonomies:

- Facts reported against concepts from the referenced taxonomy contain all the attributes that define them.

- Facts reported against concepts from the referenced taxonomy are machine-readable.

- Facts reported against concepts from the referenced taxonomy show their relationship with that taxonomy’s standard.

XBRL standard and using data from other standards

The XBRL standard provides a ready mechanism for using data from other standards. To use concepts from other taxonomies in the sustainability report, technical implementers need to include a reference to the other taxonomy. Then, a data preparer can use concepts defined in the external taxonomy, and report facts against those concepts in their reports.

Example

A company reports an annual sustainability report which needs to contain revenue figures.

Annual sustainability report (iXBRL format)

The revenue figures are available in the company’s financial report.

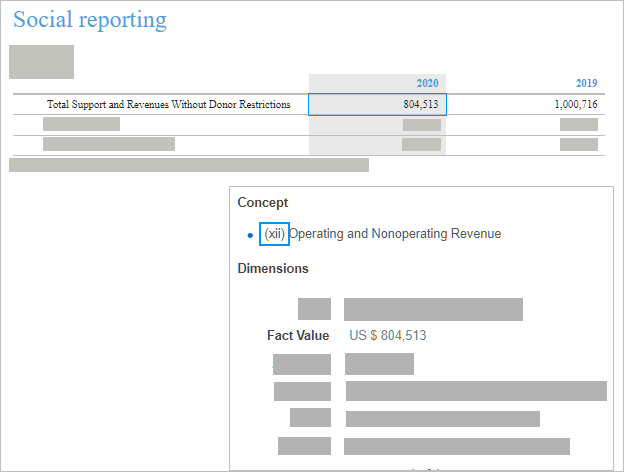

The standard setter defines that the financial data should be reported against concepts from the xii financial taxonomy. The technical implementer adds a reference to the xii taxonomy in the dsd-example-10 sustainability taxonomy.

The data preparer selects the Operating and Non-operating Revenue concept from the xii taxonomy and uses it to tag the figure in the sustainability report.

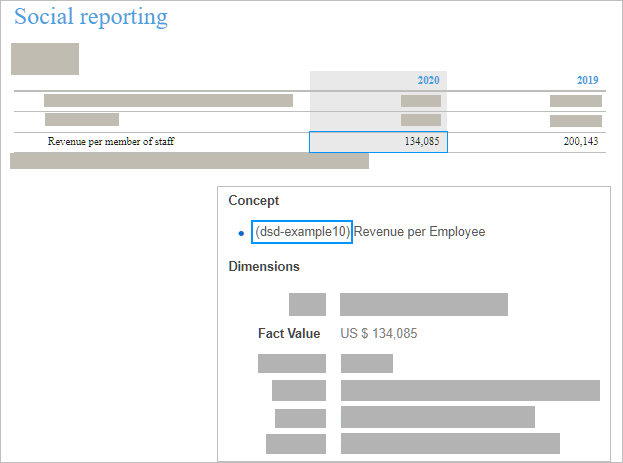

Revenue per member of staff is not reported in the financial report but is required as part of the sustainability disclosure. The data preparer selects the Revenue per Employee concept from the dsd-example-10 taxonomy and reports the data against it.

More detail

Referencing other taxonomies

Regulators, standard setters and data preparers must ensure that what is reported in the sustainability reports is both complete and accurate while minimizing the amount of work required to achieve this. The following should be taken into consideration:

- Standard setters should define which other standards should be followed when reporting particular data.

- Technical implementers should include references to external taxonomies within the sustainability taxonomy, as specified by the standard setters.

- Regulators should specify acceptable taxonomies that data preparers can use concepts from, and define how the references are added to the taxonomies.

- Data preparers should ensure that they locate the concepts they need from the referenced taxonomies to report their data.