Audited and unaudited facts

The XBRL standard enables facts in sustainability reports to be marked as audited or unaudited.

Sustainability reports can be audited to ensure the data in the report is correct and can be trusted. There may be one or more auditors of a report and each auditor may audit a number of different items.

Sometimes the auditors audit the whole document, or their audit can be at the level of a fact, a section, a page, or a table. The audit level can depend on the specialisation of different auditors.

XBRL standard and marking data as audited or unaudited

In Inline XBRL (iXBRL), it is possible to create fact-to-fact relationships by using links and use this mechanism to mark facts as audited. An audited fact points to the auditor of that fact and the auditor fact in turn lists the associated audited facts. Unaudited facts can be processed in a similar way.

Data preparers can create a fact for each auditor and then link the audited sustainability facts to that auditor fact. This relationship is marked in a footnote in the sustainability data fact.

Learn more about linking within reports

Example

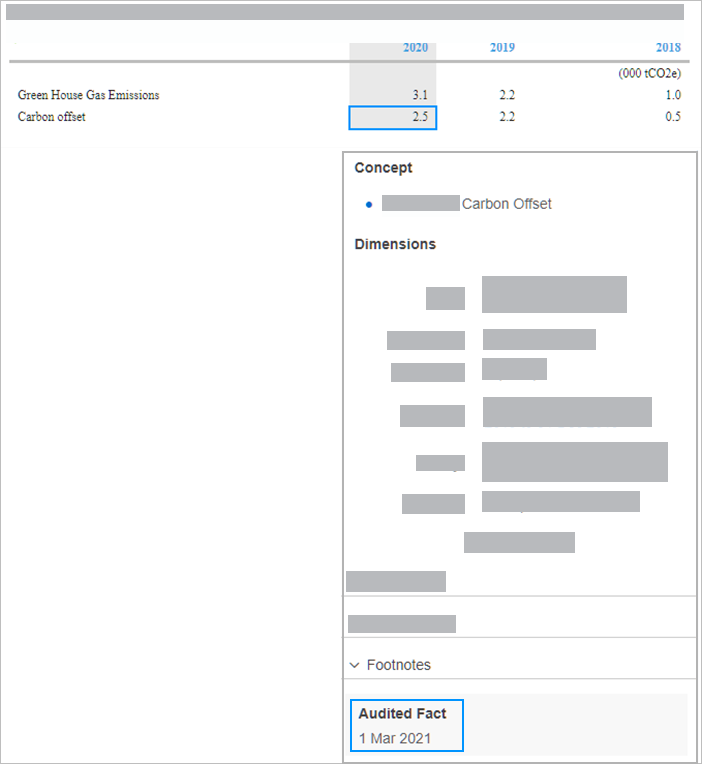

A company, Carmaker, reports its greenhouse gas emissions, which contains tables of sustainability data.

CarMaker report (iXBRL format)

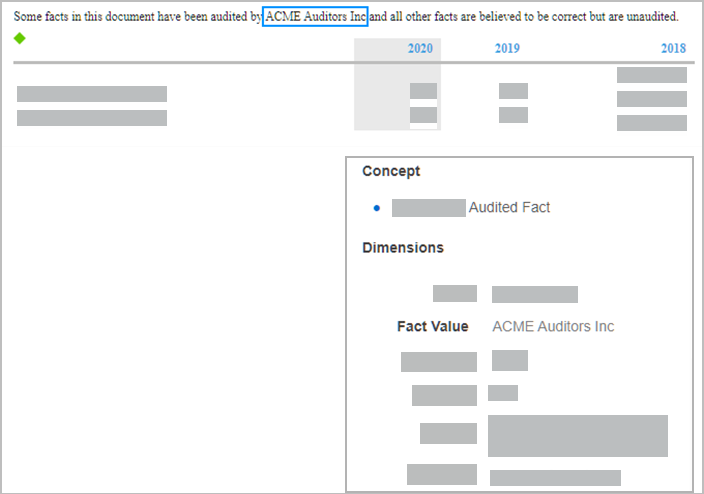

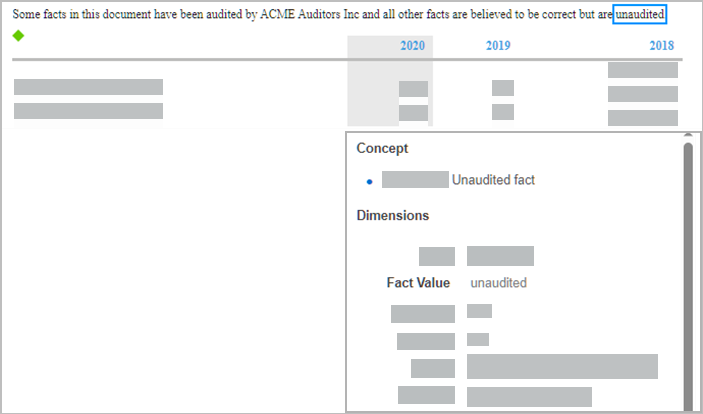

The company’s report is audited, and the auditors’ report states which facts are audited and which are unaudited.

For audited facts, the data preparer creates multiple Audited Fact facts, one for each auditor with the Fact Value containing the auditor’s name. For unaudited facts, the data preparer creates one Unaudited Fact fact.

Whenever the auditor approves a fact, the audited fact is linked to the auditor’s fact.

The Audited Fact marker in the footnote links to the auditor fact.

It is possible to view all the facts that were audited by an auditor in the Associated facts section of the auditor’s fact.

More detail

Marking facts as audited

Standard setters and regulators must decide whether reports should be audited or not. If reports need to be audited, the following must be considered:

- Standard setters must decide at what level the auditing process is done.

The level should be determined so data consumers have confidence in the information presented. - Standard setters and technical implementers should determine the linking method for audited facts.

It is only possible to link between facts. If an audit is done at the granularity of a table cell, each table cell is its own fact and linking those facts with the audit fact is simple. If an audit is done at the granularity of an entire table, rather than the table cell level, then a taxonomy concept will be needed for the entire table so that a fact for the table can be created, to use as the destination for the link from any auditor fact. - Data preparers should keep in mind that audited facts will need to be linked to auditors when preparing the sustainability reports.